Households actively shopping for a planner

Households actively shopping for a planner · Divorce planning

Understand what planners do, what it costs, and which moves you can DIY first.

Net Pay Estimator

Illustrative$15,953

Federal

$7,480

State

$8,415

FICA

29%

Eff. Rate

Illustrative estimate only — not tax advice. Uses simplified 2025 federal brackets and estimated state effective rates. Verify with a licensed CPA or tax professional.

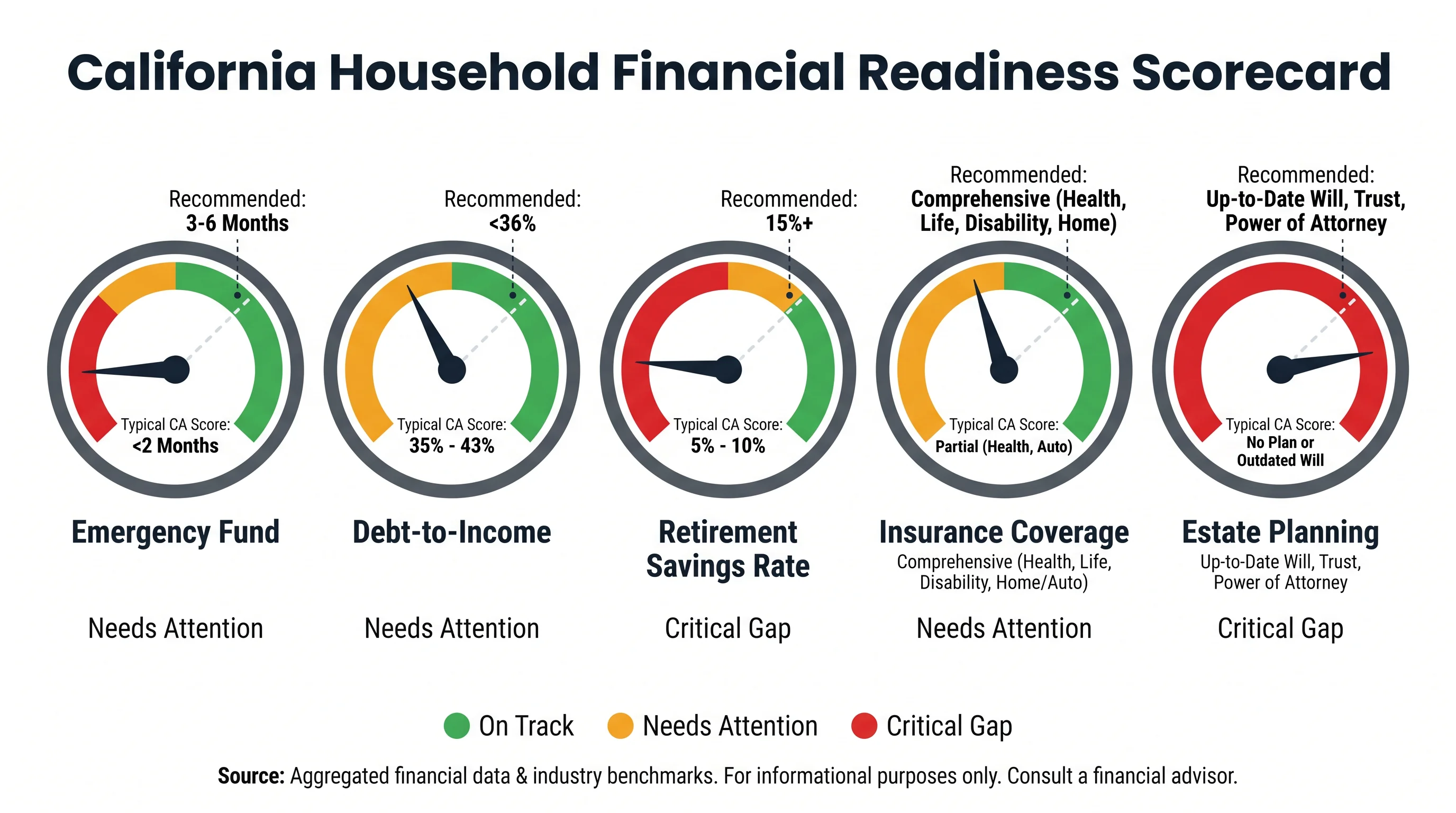

California household financial readiness scorecard — Illustrative. Not financial advice.

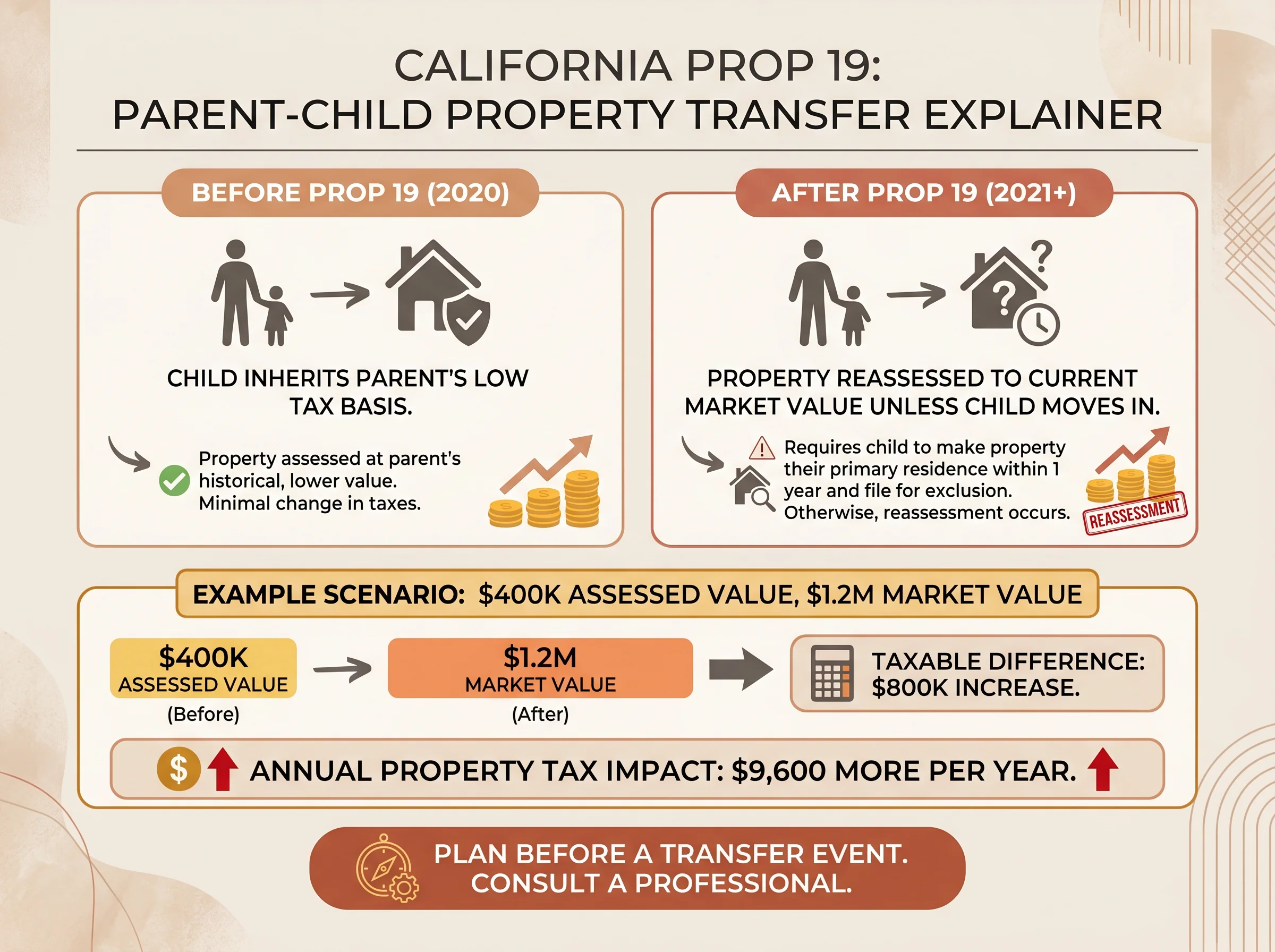

California Prop 19 — parent-child property transfer impact — Illustrative.

What We Cover

Cash flow, net worth, and retirement income modeling for CA families

Affordability analysis, property tax planning, and Prop 19 strategy

Social Security optimization, Roth conversion ladders, and RMDs

Risk-aligned portfolio construction with CA tax-efficiency lens

Community property, living trusts, and beneficiary optimization

California Retirement Planning

State income tax on all retirement distributions, high property values, and Prop 19 implications for passing wealth to the next generation make California retirement one of the most planning-intensive in the country.

Use the retirement readiness scorecard

De-risk the planner shopping journey while teaching execution.

financialplannercalifornia.com is a standalone planner-brand publication: built for Californians who are comparing planning approaches, understanding fee models, and executing the basics before they hire anyone. It has its own IA, its own examples, and its own SERP targets. Calculators ship with planner-specific framing — goals, milestones, ethics. Advisory remains optional and gated.

Households actively shopping for a planner · Divorce planning

DIYers deciding if they need help · Small-business owners separating books

Recently relocated professionals · Windfall recipients

In practice

Own the “financial planner California” intent with hyper-practical guides, checklists, and calculators that monetize via ads and membership while reserving licensed planning conversations for a structured $99 path. financialplannercalifornia.com is a standalone planner-brand publication: built for Californians who are comparing planning approaches, understanding fee models, and executing the basics before they hire a

Featured tools

Planner-language outputs, fee-ethics context, and California milestone examples — purpose-built for the planner-shopping journey, not generic household finance.

Interactive

Planner-language outputs, fee-ethics context, and California milestone examples — purpose-built for the planner-shopping journey, not generic household finance.

Future value

$1,185,264

Projected ending balance under the current compounding path.

Your contributions

$460,000

Starting capital plus every monthly contribution.

Investment growth

$725,264

The share created by compounding instead of deposits.

Output path

The line updates immediately as you change the assumptions.

Year 0 to Year 20

Interactive

Planner-language outputs, fee-ethics context, and California milestone examples — purpose-built for the planner-shopping journey, not generic household finance.

Enter current and target weights. The model normalizes them to 100% and flags any sleeve that sits outside your drift band.

equities

fixed Income

alternatives

cash

Largest sleeve

55%

Anything too dominant deserves extra governance.

Effective sleeves

2.6

A lower value means the portfolio behaves like fewer real bets.

Concentration score

0.39

Herfindahl-style concentration across the current weights.

equities

Current 55% vs target 60%

Drift: -5%. Keep this sleeve within +/-5% to stay inside the current policy.

fixed Income

Current 25% vs target 20%

Drift: 5%. Keep this sleeve within +/-5% to stay inside the current policy.

alternatives

Current 10% vs target 10%

Drift: 0%. Keep this sleeve within +/-5% to stay inside the current policy.

cash

Current 10% vs target 10%

Drift: 0%. Keep this sleeve within +/-5% to stay inside the current policy.

Interactive

Planner-language outputs, fee-ethics context, and California milestone examples — purpose-built for the planner-shopping journey, not generic household finance.

Nominal balance

$3M

Raw dollars at the retirement start date.

Today's dollars

$2M

Inflation-adjusted view of the same future balance.

4% rule estimate

$130K

A quick annual draw estimate before tax planning.

Output path

The line updates immediately as you change the assumptions.

42 to 65

Sustainable real income

$112K

Approximate annual spending in today's dollars if the portfolio must last through retirement.

Membership

Reader

$0

Member

$4.99/month

Optional advisory

$99 intake

FAQ

Planner-grade clarity with household empathy—built for searches that explicitly pair “financial planner” with California life realities.

No. Materials are general education and illustration. Decisions involving securities, taxes, or planning should involve your own licensed professionals.

Remove ads and keep sessions focused for $4.99/month; premium modules roll in over time per roadmap.

How planners are featured; Sponsor policy; Privacy

De-risk the planner shopping journey while teaching execution.

Contact

This hostname must feel planner-native. Compliance and disclosures live on this property only; its design, voice, and content focus belong exclusively to the planner-shopping journey.

Great financial planning isn't just a checklist — it's a coordinated strategy. Fenul Wealth connects your income plan, tax position, and estate goals into a single, actionable framework.

Opens fenulwealthmanagement.com · General education only · No fiduciary relationship formed on this page